For Succession Real Estate Partner Len Rifkind, real estate is more than an asset class—it is a multigenerational legacy. His grandfather, George Baker, arrived at Angel Island in 1932 with no English, no connections, and a disabled arm. Within two decades, he became a successful Bay Area developer, building subdivisions, apartments, gas stations, and retail properties. His determination not only established the family’s foothold in the United States but also shaped an investment ethos carried forward by his daughter and son-in-law, Joyce and Gary Rifkind, both accomplished real estate investors and community leaders.

Len followed in their footsteps, spending thirty-seven years as a real estate attorney and investor, ultimately partnering with Kirk McKinney and later Jeff Farnsworth to acquire more than 110,000 square feet of commercial property. Yet even for a family with deep expertise, the transition of a long-held portfolio brought significant complexity.

In 2024, after Len’s father passed and his mother was no longer able to manage the portfolio actively, the family faced questions familiar to many high-net-worth families:

How do we reduce management burdens without diminishing returns? How do we mitigate risk? How do we make decisions that strengthen, rather than strain, family relationships?

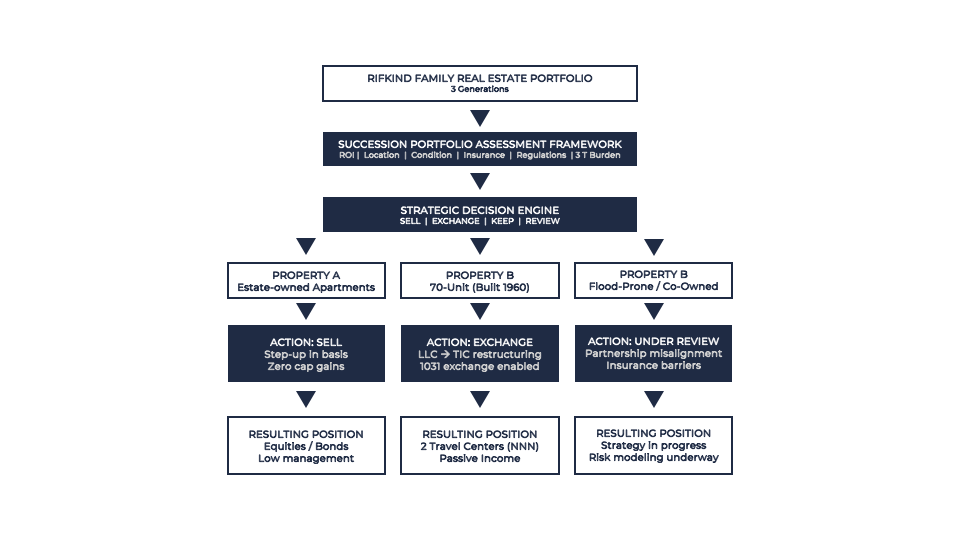

Recognizing the need for a clear plan, Len engaged Kirk and Jeff to form Succession Real Estate, a firm dedicated to guiding families through precisely these transitions. The team worked with the Rifkind family to design a comprehensive succession strategy grounded in objective criteria: property performance and ROI, location quality, required capital improvements, insurance availability, regulatory exposure, and the ever-present “three T’s”—toilets, tenants, and trash.

Strategic Outcomes

Through Succession’s structured evaluation process, three apartment buildings within the portfolio required different paths:

- Building 1 – Sale and Reinvestment:

A property owned solely by Gary’s estate was sold immediately following his passing. The step-up in basis allowed the family to avoid capital gains tax, and the proceeds were reinvested with a New York advisor into diversified, low-maintenance assets. - Building 2 – Tax-Efficient Exchange and Enhanced Returns:

A 70-unit apartment building developed by George Baker in 1960 and co-owned by four family branches was restructured from an LLC to a tenant-in-common structure to enable the respective families to exchange, avoid capital gains tax, and reinvest separately. The Rifkind’s exchanged their share into two large travel centers under long-term triple-net leases,doubling their return on investment while eliminating day-to-day management demands. After managing this building for 30 years, Len considers this one of the most successful outcomes of the planning process. - Building 3 – Ongoing Evaluation:

A property in a vulnerable neighborhood prone to flooding, co-owned with a partner at 50% without a formal agreement, remains under strategic review. Succession is guiding risk exposure, owner alignment, and potential resolution options.

The family’s commercial strip center, complicated by environmental issues from a 1950s gas station, is also being evaluated with an eye toward long-term stabilization or disposition.

Impact

Succession Real Estate’s work enabled the Rifkind family to:

- Reduce management responsibilities

- Reallocate assets into higher-performing, lower-risk holdings

- Resolve intergenerational differences with clarity and consensus

- Preserve the family legacy while positioning the portfolio for future generations

If your family faces similar decisions—or would benefit from an experienced, discreet partner to help evaluate your portfolio—Succession Real Estate stands ready to help.

For more on this topic, contact Kirk McKinney, Principal, at 415-254-2517 or [email protected].